They say a broken mirror earns you seven years of bad luck. That makes sense—something bad yields something bad.

Then why do we so often say in finance that when something bad happens it is good for the markets? In fact, it seems that we will often go weeks, even months, saying bad news is considered good news for stocks?

I guess it’s like that old saying: “What’s bad for the worm is good for the bird.” The bad fortune of one turns into the good fortune of another. Life’s full of these little ironies.

In the financial world, I think there are no bad events, just new opportunities. If life gives you lemons, you make lemonade.

We all know that the stock market consists of both peaks and valleys (in fact, all markets do). Successful investors view the valleys as opportunity zones. As long as the valleys don’t turn out to be the Grand Canyon (deep valleys that can take ages to get through), you can do very well by buying on the bad news. This is the foundation of a whole school of investing—the value-investing credo of the would-be Warren Buffetts of the world.

Dynamic, risk-managed investing aims to help investors avoid the market’s “Grand Canyons.” And if the valley turns out not to be the Grand Canyon, dynamic, risk-managed investing seeks to keep you invested to gain the benefits of the ride up to higher ground.

Or, you could try another investment approach: buy and hold. This approach is based on the premise that the principal asset classes (stocks, bonds, and gold) make money over time. Therefore, you just have to invest, hold on, and enjoy the eventual benefits. However, when you drive down into that inevitable Grand Canyon (historically, they come along every five to 10 years on average), “buy and hold” forces you to stay the course despite the risk, taking potentially deep losses until the world rights itself again.

It’s like Ernest Hemingway once said, “A man’s got to take a lot of punishment to write a really funny book.”

Over the years, I’ve wondered about the investors that market gurus and academics assume can sit through a 50%–75% decline (this happened twice over the last 20 years) and then wait three to seven years for the markets to return to breakeven. They must have wills of steel and the patience of Job.

Most investors I know can’t stomach the volatility. Yet, they need the exposure to the markets to build for their future.

Dynamic, risk-managed investing was developed for these investors. It seeks to mitigate losses during these major market disruptions. It aims to lose less or even profit when the market takes these 50%-plus descents and preserve more cash to invest with when the market starts to gain ground again.

Of course, we aren’t always experiencing a bear market. When the market is trending higher, everyone can make money.

But even though dynamic risk management is made for the Grand Canyon–type investment excursion, there are smaller peaks and valleys that occur between the major up- and downtrends. This is the most difficult time for dynamic risk management.

When the market has a series of 5% moves up and down (2011, 2015, or even the double-dip volatility of 2018), going nowhere for a quarter or two, it can be frustrating even though it is not as costly as the super bear markets we talked about last week.

These “sideways markets” force risk managers to take one of two courses: (1) They can have intermediate-term strategies that are not as sensitive to market movements so as not to get whipsawed by small or sudden market gyrations. (2) They can develop shorter-term daily trading models designed to take advantage of such movements.

Both types deserve a place in truly diversified investor portfolios, especially during those times when something bad in the world equals something good for investors.

Market update

Last week we began one of those “bad times are good times” periods in the stock market. Trade threats on two continents, disappointing earnings and economic reports, and disruptive politics were all the talk on the financial news networks and in the investment publications. So what did stocks do?

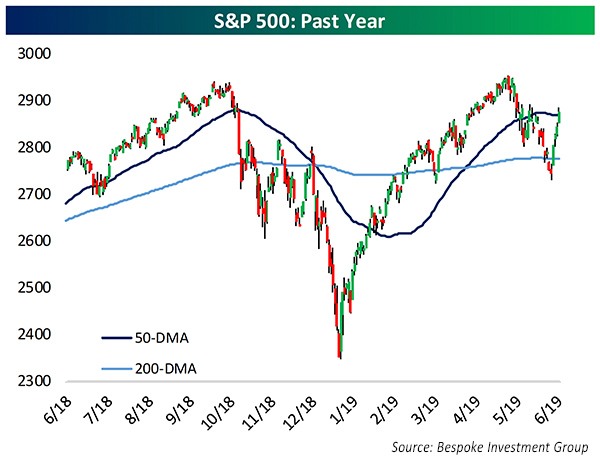

The stock indexes rose for five straight days. The staid Dow Jones Industrial Average gained over 1,100 points. The NASDAQ, despite investigation and antitrust threats to its biggest members, shot up 3.9% higher. The S&P rocketed over 4.4% and topped both its 50-day and 200-day moving averages.

Why this seemingly backward behavior?

Markets deemed a threat to the economy as bad news. Their belief was that the economy was slowing down. That was bad news, but it was good news.

The markets are currently betting that the Federal Reserve will respond to the economic slowdown by lowering short-term interest rates. According to the prognosticators’ reading of the interest-rate tea leaves, the chance of an interest-rate reduction at the July meeting this year is more than 85%. (For the record, just months ago the perception was that the Fed would increase rates, which didn’t happen.)

Lower interest rates mean more opportunities for businesses to leverage their opportunities. Finally, an equation that makes sense: What’s good for business is good for stocks.

However, until last week, Wall Street seemed not to notice that bond investors have been getting ahead of the Fed. They have lowered rates already without waiting for Fed action. As a result, the lower interest-rate environment that the bad news should have caused has already come to pass. We are there already whether or not the Fed acts at or before its next meeting.

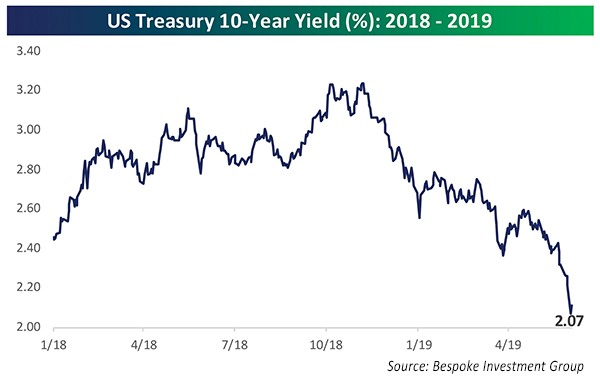

As long as these low rates continue, there will be a strong foundation for a continual rise in stock prices. With the 10-year Treasury bond yielding 2.07%, the S&P closed on Friday with a dividend yield of 2.02%. Which seems more likely to yield a higher return in the intermediate-term future? When this has happened in the past, it has been good for bonds—but even more so for stocks.

Stocks have already recovered a third of their May losses (based on the S&P). The S&P 500 closed on Monday (6/10) within 2.4% of its all-time high. More than 10% of stocks on the New York Stock Exchange have already exceeded their 52-week highs, and that’s just days after the S&P registered its lowest level in 50 days (usually a buy signal that is good for at least a month).

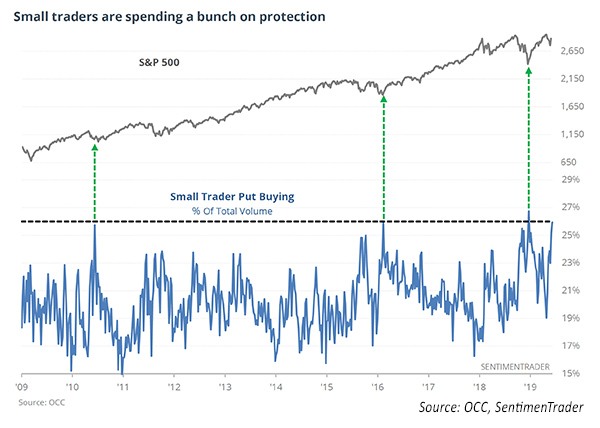

Still, as of Friday (6/7), investors have not only shrugged their collective shoulders but they have also taken more money off the equity table. The AAII (American Association of Individual Investors) and Investors Intelligence Sentiment surveys are recording their lowest bullish, and highest bearish, readings since the December 2018 bottom was made in stocks.

As last week ended, options being bought by small investors were overwhelmingly betting on a lower market. These actions are not normally seen at market tops.

Sixty-six million years ago, an enormous asteroid flamed through the earth’s atmosphere, hitting the planet surface with an impact greater than any hydrogen bomb. The result was bad for the dinosaurs … but it was good for humans.

Disclosure: No communication by Dynamic Performance Publishing or our employees to you should be deemed as personalized investment advice. Any investment recommended in this newsletter should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company. Dynamic Performance Publishing, its affiliates, and clients may hold positions in the recommended securities. Results are not indicative of holdings for clients of Flexible Plan Investments. Forwarding, copying, or otherwise duplicating this information for the use by anyone other than the intended recipient is expressly forbidden. These results are not representative of those achieved by clients of Flexible Plan Investments, Ltd. (FPI) due to differences in security selection, timing of trades, transaction fees, and FPI’s management fees.