Barclays yesterday (9/1/2010) launched the Barclays ETN+ S&P VEQTOR ETN (VQT) exchange-traded notes (ETNs) that are linked to the performance of the S&P 500 Dynamic VEQTOR Total Return Index (press release).

Barclays takes “dynamic indexing” to a new level with VQT. The underlying index can be dramatically reconfigured on a daily basis and employs a stop-loss mechanism. The underlying index seeks to provide broad U.S. equity market exposure with an implied volatility hedge. It will dynamically allocate investments among three components: equity (S&P 500 Total Return Index), volatility (S&P 500 VIX Short-Term Futures Index), and cash.

The VQT overview page and VQT fact sheet (pdf) provide the investment philosophy behind this product:

“the volatility component of the Index is premised on the observation that, historically, volatility in the equity markets tends to correlate negatively to the performance of US equity markets. In addition, rapid declines in the performance of the US equity markets generally tend to be associated with particularly high volatility in such markets. The Index, therefore, seeks to reflect such historically observed trends by allocating a greater proportion of its notional value to investments in the US equity markets during periods of low market volatility with the ability to allocate a greater proportion of its notional value to investments in a reference asset that tracks implied volatility during periods of high market volatility. The Index also incorporates a “stop loss” mechanic that shifts the entire value of the Index to an interest-bearing cash investment under certain circumstances.”

The S&P 500 Dynamic VEQTOR Total Return Index

Barclays has demonstrated its ability to design and deliver products that can accurately track an index after fees (a 0.95% investor fee in this case), so the key to understanding VQT is to understand the index.

On any index business day, the index allocates weightings to the equity and volatility components based on a combination of realized and implied volatility. The maximum weighting of the volatility component is 40%, and the combination of the equity and volatility components are typically 100% of the notional value of the index (no leverage) and 0% if a stop-loss event has occurred.

The stop-loss feature will allocate into a 100% cash position if the value of the Index has fallen greater than or equal to 2% over the preceding five days. Since the stop-loss criteria is determined from the index itself, the move to cash can be as short as one day and a maximum of five days since being in cash for five days guarantees that the five-day return is greater than a 2% loss.

Index calculation is a 4-step process:

- Determine the Realized Volatility

- Determine the Implied Volatility Trend

- Determine the Target Weightings of the Equity Component and Volatility Component

- Evaluate Whether a Stop Loss Event Has Occurred

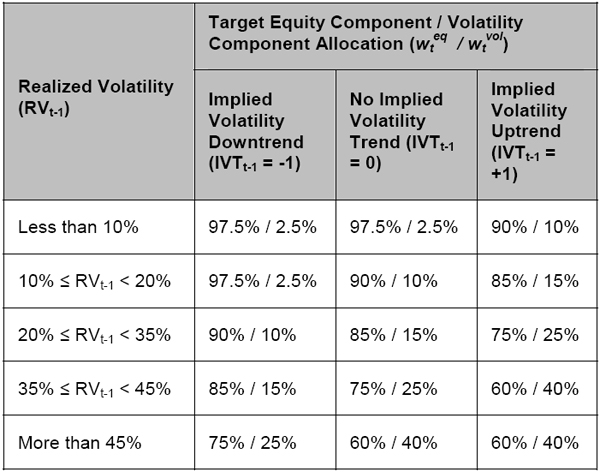

The following table is part of the prospectus and shows the 15 combinations of realized and implied volatility and the resulting allocation between the equity and volatility components.

When not in a cash override stop-loss condition, the volatility component can range from a low of 2.5% to a maximum of 40%. Additional details on the index calculation methodology are in the VQT prospectus and pricing supplement (pdf).

Investors could potentially implement this strategy on their own using the SPDR S&P 500 (SPY) and iPath S&P 500 VIX Short-Term Futures ETN (VXX), but I wouldn’t recommend it. The daily slippage, commissions, and overnight gaps are likely to induce extreme tracking error into any do-it-yourself implementation, not to mention the time and effort involved.

VQT has the potential to be a great product. Investor education is likely to be the largest hurdle at this time, and I would advise anyone to understand this product before buying it. It also has the negative characteristic of credit risk that comes with all ETNs. Barclays also needs to work on a consistent marketing message because once again they avoided the iPath brand for VQT.

Disclosure covering writer, editor, and publisher: No positions in any of the securities mentioned. No positions in any of the companies or ETF sponsors mentioned. No income, revenue, or other compensation (either directly or indirectly) received from, or on behalf of, any of the companies or ETF sponsors mentioned.