Much has been written about the math behind leveraged ETFs and mutual funds, yet most investors fail to realize the true impact. As a result, many of these products have been ridiculed for failing to meet user expectations.

Much has been written about the math behind leveraged ETFs and mutual funds, yet most investors fail to realize the true impact. As a result, many of these products have been ridiculed for failing to meet user expectations.

Contrary to popular belief, leveraged and inverse products that reset their exposure level every day are not new. Rydex introduced the concept with the launch of Rydex Nova (RYNVX) in 1993 and Rydex Ursa (RYURX) in 1994 (note: Ursa has since been renamed Rydex Inverse S&P 500 Strategy).

However, as more and more leverage is applied in these products, the adverse impacts appear to grow exponentially. Direxion introduced 3x ETFs in late 2008, and now we have five months of data to look at.

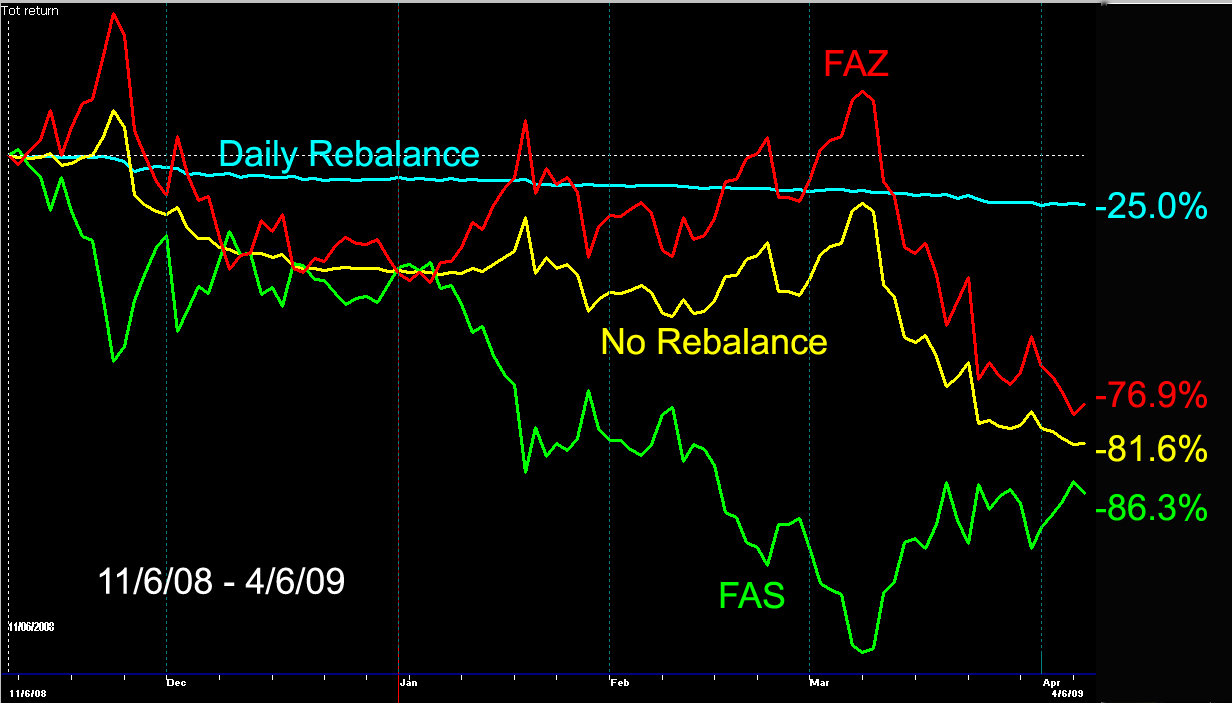

For this example, I have chosen two inversely related leveraged funds: Direxion Financial Bull 3x Shares (FAS) and Direxion Financial Bear 3x Shares (FAZ). The chart below illustrates the returns for the five-month period from 11/6/2008 through 4/6/2009 for the following four scenarios:

- Green Line: Buy and hold FAS = -86.3%

- Red Line: Buy and hold FAZ = -76.9%

- Yellow Line: Buy and hold equal amounts of FAS and FAZ with no rebalancing (what some might consider a perfect hedge) = -81.6%

- Cyan Line: Buy equal amounts of FAS and FAZ and rebalance every day (a lot of work) = -25.0% (not counting transaction fees and slippage)

Chart and data by www.FastTrack.net

Even if you go to the trouble of rebalancing every single day the market is open, you are still fighting a headwind of 25% for a five-month period. Most people would consider that impossible to overcome on any kind of continuing basis.

I’ve said it before and I’ll say it again: Leveraged ETFs can be great short-term trading instruments, but make sure you understand the longer-term impact before holding any of them for more than a few days.

All the ETF sponsors of leveraged and inverse products provide warnings and educational material. Here are links to such information for DirexionShares, ProShares, and RydexShares.

Disclosure: no positions