The phrase “active management” no longer conveys what was originally intended. Once it was a strategy to contrast with the “buy-and-hope investing strategy.” Today, active management conveys a brand of investing practiced by traditional mutual funds. It is contrasted with passive investing. Yet, in reality, there is little difference. The two have blended to the point where you cannot discern which is which.

Traditional mutual fund investing is governed by an investment committee that usually follows a bottom-up approach to investing. They may actively search for candidates for their buys and sells, but once they buy, it’s often a long time before they sell. And what they buy is constrained by the limitations of their strictly defined prospectus.

In the same way, a passive investing approach usually follows the strict confines of a predefined index. But it doesn’t buy and hold that either. Each year or so, changes are made to the index when an investment management committee deems it wise. Sound familiar?

It’s pretty much the same approach, isn’t it? Yet one is called “active” and the other “passive.”

There are two differences. The first is the holding period of the buys of each. The so-called active approach can sell at any time. The passive indexed approach only sells on a predetermined rebalancing date. This leads to greater turnover in the “active” approach but often a lower downside when the market goes down.

And that takes us to the other difference: cost. With less trading, less monitoring, and—let’s just say it—less effort and work, the passive approach can reduce the cost of the end product.

To top it off, the passive investing crowd has pulled off a bit of legerdemain, or sleight of hand. They now index active manager methodologies and then call them passive because they follow a set of predefined rules! Despite these rules being active management rules, the ETF providers marketing them call them “passive.”

Of course, there are now “active” ETFs. How are they managed? Since most come from mutual fund managers, they mirror their “actively managed” mutual funds.

If this all sounds a bit circular, like the great snake consuming its own tail, it’s because that’s the state of the industry.

So I’ve had it. I don’t want to be, or be called, an active manager anymore!

I dynamically risk manage my client portfolios. So that makes me a dynamic risk manager instead.

I manage “dynamically.” That means that I’m not tied to a calendar when it comes to trading. I can be responsive to the markets. I can change my whole approach to trading on a dime because the applicable economic regime has changed, or the market technicals have weakened. I eschew the “buy-and-hope approach.”

Further, I don’t have to buy all of the stocks in an index. I can avoid the laggards and hold the leaders. I can carefully monitor and groom my portfolios rather than sticking with a holding just because it came with an index.

And I’m also unconstrained by a restrictive prospectus. In my separately managed accounts, I seek out opportunities wherever I may find them.

In addition to being dynamic, I am also a “risk manager.” In contrast with traditional mutual funds, and certainly the passive indexers, my first instinct is to control risk.

Why? We’ve all witnessed it. When the markets tumble, the indexes and traditional mutual funds all seem to fall as well. When the train is on the track and barreling straight for them, they make no effort to get out of the way. Their modus operandi is to sustain the loss, clear the wreckage, and hold fast.

A risk manager should do more. He or she should monitor and select investment strategies with a view to their volatility, in addition to their return. Cost is a factor, but the stated returns that all investment advisors must show are already net of those costs.

Yes, the risk manager is doing a great deal more than the passive indexer, for which they should be paid, but the real differentiator is not cost. It’s how well the strategy works at achieving the investor’s goals. If the return is higher, the drawdown lower, or the fit is better to the client’s return and risk appetite, then, since the expense ratio and the trading costs are already accounted for in the performance shown, these should not be the only factors considered when choosing an investment strategy.

Market update

Stocks headed higher for a second week in a row. The leading indexes for stocks tended to be the small-cap variety. While the rising trend of stocks in general seems to belie any concern with the trade war that commenced last week, the continued strength in small caps, which are less dependent on international revenues, suggests that there is at least a hint of worry.

There was little to concern stock investors from a technical perspective. The advance-decline line, generally viewed as the best indicator of market breadth, continued to move higher, making a new all-time high on Friday. While the S&P failed to make a new high, the S&P tends to follow the broader market higher in these instances.

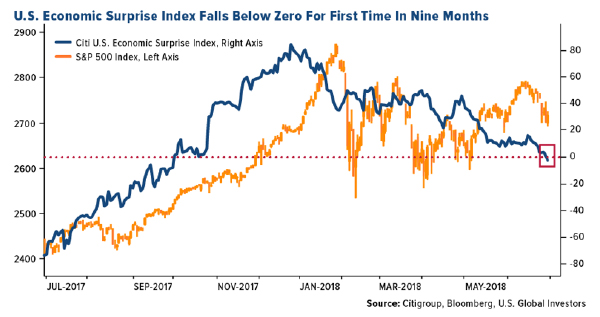

Economic reports have not been surprising to the upside like they were just months ago. In fact, there has been such a dearth of positive surprises that the Citi Economic Surprise Index turned negative last week. Historically, this has suggested the coming of some stock market weakness over the next six months.

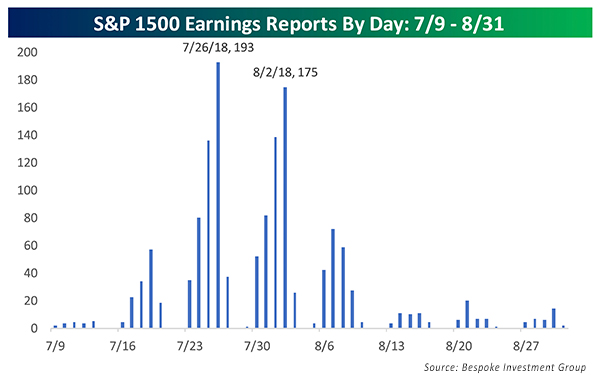

At least for the immediate future, however, it seems economic reports are not what most investors are on the lookout for. As the next chart shows, the reporting season for second-quarter earnings is upon us.

There is not much going on this week, although major banks may supply some surprises. The real action is still two to three weeks away. Yet most of the financial chatter seems to be already focused on the reports.

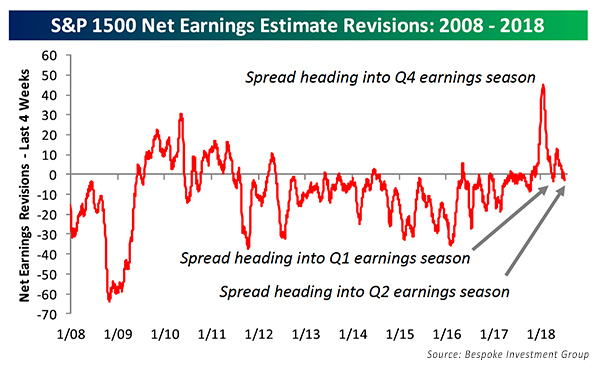

Earnings revisions by earnings analysts have been mostly negative going into this season. Just a month ago, however, the period was viewed much more positively.

The pessimistic pivot is actually positive for stocks. Bespoke Investment Group has reported that when analysts are negative going into earnings season, stocks have historically risen, on average. Although the level of negativity is not great this time around, Bespoke reports that the current level has given a 2% positive return edge by the end of reporting with gains nine out of 10 times.

Seasonality is good for stocks in July, although after the Fourth-of-July-week gains, it is quieter until midmonth.

Bond yields fell a bit last week, providing some gains to the various bond market indexes. It also lent support to rallying stocks.

I note that bitcoin remains weak despite a recent blip upward. At about $6,700 per coin, it’s come down quite a ways since my sell signal back in early December as it neared $20,000.

It’s easy to see why, considering this report from U.S. Global Investors:

“In its initial quarterly report on coin theft, CipherTrace (a California-based blockchain security firm) reported that in the first half of the year, more than $760 million in cryptocurrency was stolen from exchanges. That’s almost three times more than in all of 2017, Bloomberg reports. ‘This overall market expansion has created a whole new generation of cyber criminals that didn’t exist 15 months ago,’ CEO of CipherTrace said in a phone interview.”

Just what we needed!

Disclosure: No communication by Dynamic Performance Publishing or our employees to you should be deemed as personalized investment advice. Any investment recommended in this newsletter should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company. Dynamic Performance Publishing, its affiliates, and clients may hold positions in the recommended securities. Results are not indicative of holdings for clients of Flexible Plan Investments. Forwarding, copying, or otherwise duplicating this information for the use by anyone other than the intended recipient is expressly forbidden. These results are not representative of those achieved by clients of Flexible Plan Investments, Ltd. (FPI) due to differences in security selection, timing of trades, transaction fees, and FPI’s management fees.