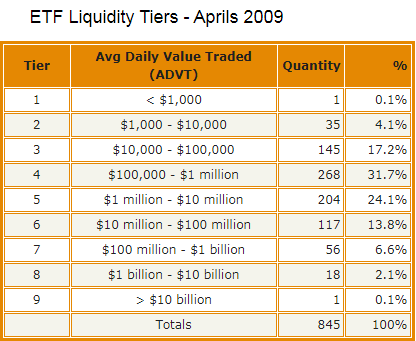

The overall look and feel of this month’s liquidity tier table is much like the one from last month. If plotted it would have the general appearance of a bell curve. There are a total of nine tiers, with each one representing an order of magnitude improvement in the Average Daily Value Traded (ADVT).

The overall look and feel of this month’s liquidity tier table is much like the one from last month. If plotted it would have the general appearance of a bell curve. There are a total of nine tiers, with each one representing an order of magnitude improvement in the Average Daily Value Traded (ADVT).

Tier 4, ETFs trading between $100,000 and $1 million per day, is once again the largest. More than 30% of the ETFs and ETNs fall into this category. Trading activity in this tier is often spotty, sometimes with only a few trades per day. Traders should generally avoid these ETFs while investors should use limit orders.

The three lower tiers have 181 members, including all the funds that are on ETF Deathwatch and new ETFs that have yet to establish a foothold. When combined with Tier 4, these lower tiers represent the majority (53.1%) of all ETFs. In other words, the majority of ETFs have liquidity concerns. Additional information on ETF liquidity can be found in the March issue of ETF Liquidity Tiers.

Tiers 5, 6, and 7 represent increasing volume and value traded. The bid/ask spreads are supported by deeper volume, and market makers are usually keeping an eye on trading price versus indicative value. Depending on the size of your trades, market orders start to become a reasonable option for the 377 ETFs in these tiers. This month’s combined count is nearly the same as last month’s 373.

Tiers 8 and 9 represent the best of the ETF world in terms of liquidity. These are the members of the ETF Billion Dollar Club – the ETFs that garner the lion’s share of ETF trading. There are only 19 ETFs in these two tiers, just 2% of all U.S. listed ETFs, but they accounted for more than 76% of all ETF value traded in the month of March.

The following table shows each liquidity tier based on Average Daily Value Traded (ADVT), along with the number of ETFs and the percentage of the ETF population that make up that tier.

Note: this table is constructed from data supplied by Premium Data comprising all U.S. listed ETFs and ETNs during the month of March (839 active at the end of the month plus six closures during the month). The data for new ETFs and ETF closures has been pro-rated.

Unlike stocks, ETFs have a creation/redemption process that allows the creation of new shares to meet increased demand. Likewise, ETF shares can be retired (redeemed) when demand wanes. This increases ETF liquidity far beyond the level of stocks with similar trading volume.

These liquidity tiers apply only to ETFs and ETNs and for comparison to other ETFs and ETNs. It is not appropriate to compare ETFs to stocks or other securities using the same scale because of the differences in liquidity factors described above.