Three years ago today, investors received their first warnings about the problems of owning MLPs inside an ETF. Unlike all the other ETFs that came before it, the Alerian MLP ETF (AMLP) from ALPS was the first ETF structured as a C-corporation and saddled with federal and state income tax liabilities. Additionally, this tax-burdened ETF chose to track the same index as the existing non-tax paying ETRACS Alerian MLP Infrastructure ETN (MLPI).

The trade seemed rather obvious: Go long MLPI while shorting an equal amount of AMLP. As a pairs trade, it is designed to capture the outperformance of MLPI while mitigating the risk of the underlying MLPs. In theory, the majority of the performance difference between the two products should amount to the tax liabilities of AMLP. Hence, I subsequently dubbed it the “Taxman Trade”.

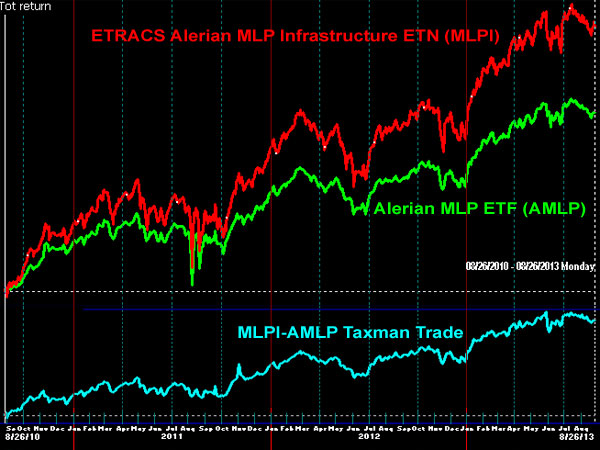

With three years of history now available, let’s check in on the Taxman Trade and see how it is doing. The following data represents the period of 8/26/2010 to 8/26/2013. Price Return was calculated from data supplied by Norgate Premium Data. Total Return was supplied by Investors FastTrack and assumes the reinvestment of all distributions.

ETRACS Alerian MLP Infrastructure ETN (MLPI)

- Price Return: +42.7% cumulative, +12.6% annualized

- Total Return: +66.0% cumulative, +18.5% annualized

Alerian MLP ETFN (AMLP)

- Price Return: +15.7% cumulative, +5.0% annualized

- Total Return: +41.1% cumulative, +12.2% annualized

Observations: Before expenses, a long MLPI short AMLP trade could have captured a +24.9% cumulative total return (+6.3% annually). ALPS likes to talk about the “tax efficiency” of AMLP, and it boldly but incorrectly proclaimed that AMLP was superior to MLPI on an after-tax basis. ALPS even requested that I retract my criticism and trade recommendation. However, the data above shows that MLPI’s price return (no distributions included) of 42.7% beat AMLP’s total return of 41.1%. Therefore, even if the tax on MLPI’s distributions were 100%, MLPI would still have beaten AMLP on an after-tax basis.

Investors and traders need to be aware that because of the daily leverage (or deleverage) employed by AMLP, this trade does not eliminate all the risk of the underlying MLPs. The MLPI notes also carry the credit risk of UBS, the issuer. The chart below shows the performance of MLPI in red, AMLP in green, and the difference in light blue. The Taxman Trade works well when MLPs are rising in value, allowing you to “collect” the taxes. When MLPs are falling in value, there is a taxable loss and the Taxman loses out.

Disclosure covering writer, editor, and publisher: No positions in any of the securities mentioned. No positions in any of the companies or ETF sponsors mentioned. No income, revenue, or other compensation (either directly or indirectly) received from, or on behalf of, any of the companies or ETF sponsors mentioned.